5 signs your business needs a multi-currency account (and how to switch)

If you sell internationally, pay remote contractors, or source suppliers abroad, you’re already operating in a global economy. But here’s the uncomfortable truth: using a standard business account to manage multiple currencies quietly erodes margin and slows momentum. Many SMEs still rely on legacy banking systems built for domestic business. That mismatch creates friction – and friction costs money.

What is a multi-currency account and why it matters

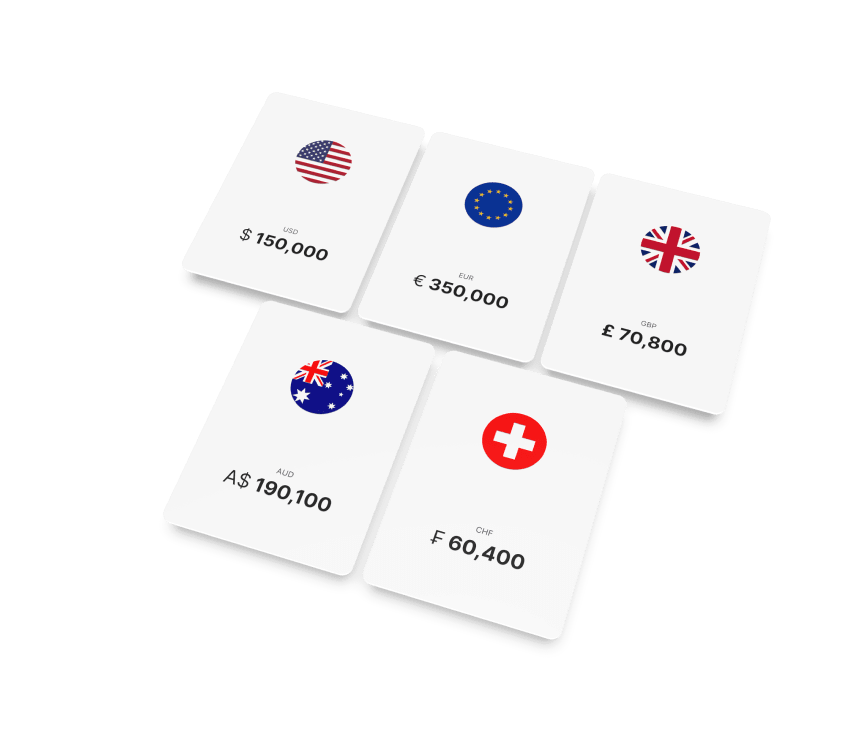

A multi-currency account allows you to receive, hold, and send funds in different currencies from a single platform. Instead of automatically converting every incoming payment into your home currency, you decide when and how the conversion happens.

That control matters. It helps minimize avoidable FX costs, allows you to time conversions more strategically, and brings clarity and stability to your cross-border cash flow.

5 signs your business needs one

- You deal with 3+ currencies every month

If you invoice clients in multiple currencies often in the same billing cycle, you’re paying conversion costs each time your bank auto-converts. That adds up quickly with regular volume.

- FX fees are eating into your profits

Traditional bank markups on foreign exchange can run well above market rates, typically ranging from 1% to 5%.

- You struggle with cash-flow timing

Holding money in local currency lets you choose when to convert. This can be a powerful hedge against sudden rate swings and gives you greater predictability over working capital.

- Reconciliation is a nightmare

Multiple bank accounts, different currency statements, and manual reconciliations create more friction and increase the risk of errors, eroding efficiency.

- Cross-border payments are slowing you down

Delays in international payments can disrupt operations and strain relationships with foreign clients and partners.

How to switch in 3 simple steps

1. Audit your currency flows

List the currencies you invoice in, pay out in, and receive most frequently. Add up the FX markups, transfer fees, and delays you’re currently absorbing. This baseline will show you exactly how much margin disappears in silent conversions and what needs fixing.

2. Choose a solution built for international business

Not all multi-currency accounts are created equal. Look for:

- Transparent FX pricing

- Support for the currencies you actually use

- Local and international payment rails

- A clear, straightforward fee structure

- Robust security features

With Satchel, you can manage 20+ currencies, access competitive exchange rates, and send or receive international payments without the friction of traditional banking layers. Instead of juggling multiple providers, you get one streamlined platform built for growing cross-border businesses.

3. Onboard and optimize

Once you’ve chosen your provider, opening a modern multi-currency account is typically fully digital and fast. Update your invoicing details, redirect incoming payments, and gradually migrate recurring supplier payouts. The gains will compound quickly.

Why it’s not just a nice-to-have

Global growth shouldn’t stall because of clunky currency conversions or outdated payment rails. Multi-currency accounts change the equation, giving businesses faster settlements, tighter cost control, and operational simplicity that legacy banking models struggle to deliver. With international transfers projected to rise by around 5% annually through 2027, investing in smarter financial infrastructure is a prerequisite for competitive advantage.